Senior Citizens Aged 75 Years and Above May Be Exempt from Filing Income Tax Returns

Understand when eligible senior citizens can avoid filing an income tax return and when the exemption does not apply.

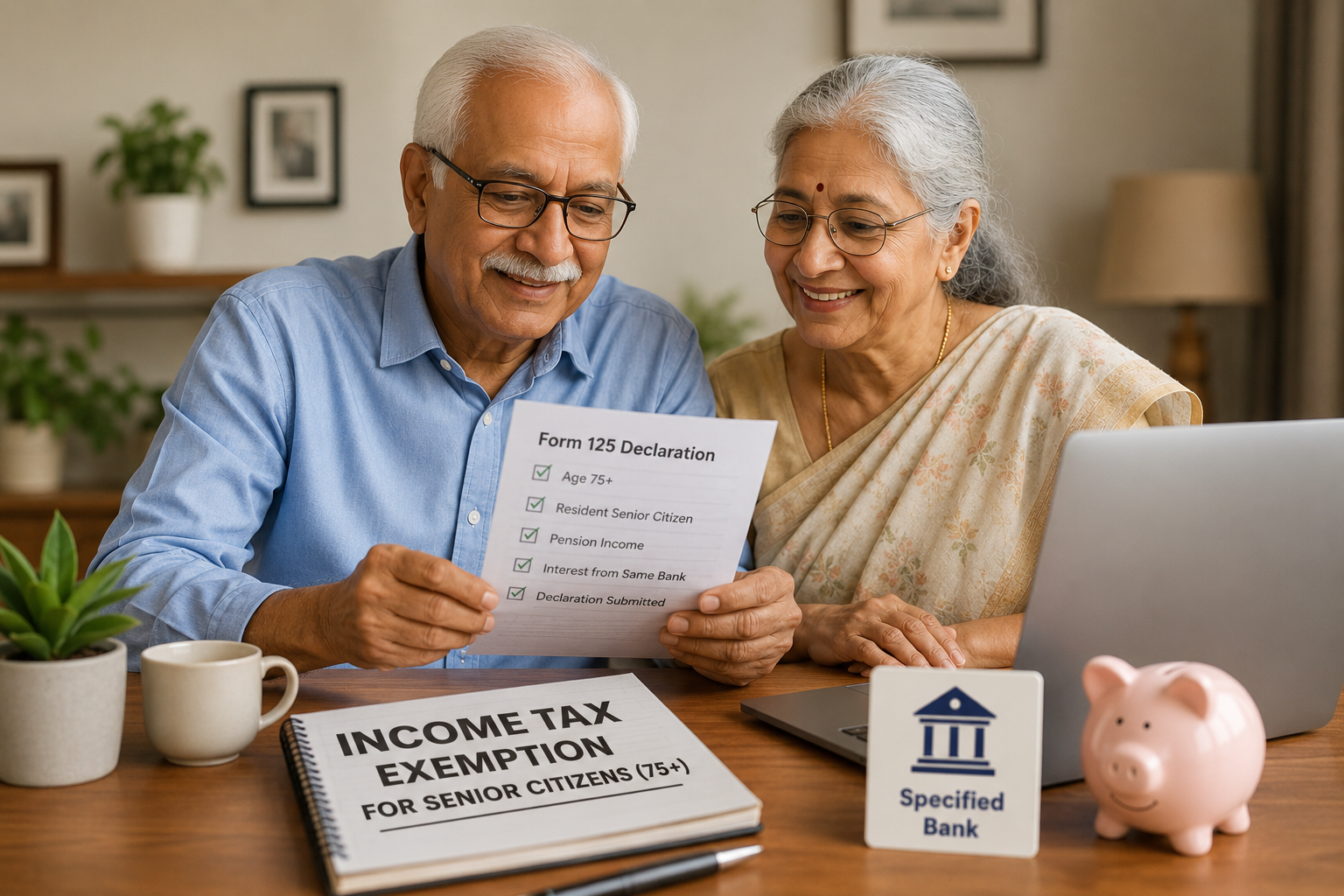

The Income-tax Act, 2025 provides a significant compliance relief for eligible senior citizens. Under Section 393(1), Serial Number 8(iii), read with Rule 208, certain resident senior citizens are exempt from filing an Income Tax Return, subject to specific conditions.

Eligibility conditions

- Age requirement: the individual must be a resident senior citizen aged 75 years or above.

- Nature of income: income should consist only of pension income and interest income from the same specified bank where the pension is received.

- Submission of declaration: the senior citizen must submit Form 125 to the specified bank.

- Specified bank requirement: the pension and interest income must be received through a bank notified by the Central Government as a specified bank.

Role of the specified bank

Once the declaration is submitted, the specified bank assumes responsibility for computing taxable income, considering eligible deductions, applying the rebate, and deducting tax at source.

Exemption from filing ITR

After the specified bank has correctly computed and deducted the tax liability, the eligible senior citizen is not required to file an Income Tax Return.

This provision is intended to simplify tax compliance for elderly taxpayers who have limited sources of income.

Important: The exemption is available only when all prescribed conditions are fulfilled. If the senior citizen has any additional source of income beyond pension and eligible interest income, the exemption may not apply.